How Housing, Economics, and Poor Financial Education Are Undermining the Middle Class

For our over-50s special edition of the Chitchat, I have decided to take a look at the changing notion of adulthood, home ownership, and marriage…

Remember when buying a house and starting a family was considered the ultimate adult achievement? For many of you over-50s, it was practically a rite of passage. You could buy a house, get married, have kids, and still find time to complain about the weather. Lucky you.

Today, those milestones are starting to look like ancient legends for Millennials. In Australia, only 55% of Millennials (25–39) own a home—compared with 62% of Generation X and 66% of Baby Boomers at the same age.

And owning it outright?

Forget it—Baby Boomers in 1991 were three times more likely to have a mortgage-free home than today’s 30-somethings.

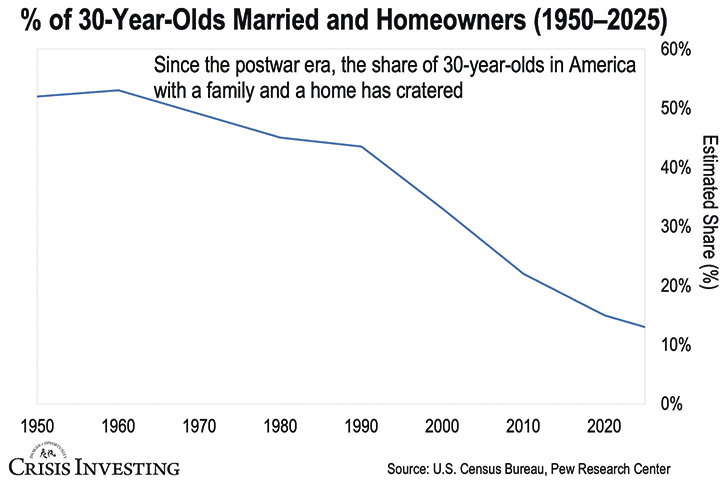

Across the U.S., the picture is even bleaker. Back in 1950, 52% of 30-year-olds were married and owned a home. By 2025, only 13% will hit both milestones. Yes, that’s a 75% collapse—basically, today’s young adults are navigating adulthood like it’s a video game set on “Impossible” mode.

What Changed?

For starters, Millennials are delaying marriage (median age 34 vs. 27 for Baby Boomers) and having fewer children—all while facing skyrocketing housing prices and mountains of debt.

Meanwhile, you lucky over-50s were cruising along with wages that actually kept up with the cost of living, cheap mortgages, and even cheaper hot chips.

This generational squeeze is happening alongside profound social changes:

• Australians reporting no religious affiliation have nearly tripled (16% → 46.5%), reshaping traditional social norms. Humanist beliefs are now covertly embedded in educational institutions.

• The share of residents born overseas has grown from 25.7% to 35.6%, influencing housing demand and community structures. New rental housing has dramatically slowed due to higher interest rates.

Together, these trends also play a part in the redefinition of what stability, adulthood, and middle-class status look like in modern Australia.

The Economic Reality

• Housing costs have long outpaced wages.

• Debt burdens are heavier than ever. In the U.S., student debt has more than doubled since 2006, leaving graduates financially constrained before buying their first home. In Australia, Higher Education Debt can lock you out of a bank loan.

• For many Australian Millennials, childless couple households are now the most common, showing how financial stress delays both homeownership and family formation.

Paradoxically, this generation is more educated, more humanist in values, and more career-driven than any before—Sadly, they are also poorer, and struggling to achieve middle class markers of success.

Why Financial Education Matters

Policy won’t fix this. While reforms to curb inflation and housing costs are critical, financial literacy is the real game-changer.

Young people need to understand where to place the blame and how to remedy the situation:

• How governments and banks influence money supply and inflation

• Fractional Reserve Banking

• How credit is created and how debt traps work

• How to save, invest, and navigate economic systems effectively

Without this knowledge, Millennials risk remaining locked out of the middle class, vulnerable to communist and fascist political ideology, and risk sliding into poverty.

The Urgent Call

The disintegration of the middle-class dream is not inevitable—but reversing it requires education, awareness, and action.

Millennials must arm themselves with financial knowledge before it’s too late, or they may find that homeownership, family formation, and economic security become relics of a past era.

Written by John E Middleclass

Chitchat Newspaper. October 2025.