DIY Super, Gold, and Property: Taking Control of Your Retirement

The Australian government has strict laws ensuring employers pay workers superannuation. It just warms your heart to know they are looking after you and ensuring you can retire with dignity. Some of you more sceptical readers may be thinking they’re really just squeezing more money out of employers and funnelling it into centralised funds their cronies manage.

But that would be very foolish of you. It’s not like they are preventing you from accessing your money, creating hundreds of pages of rules around what you can do with your money, or making pesky SMSF investors jump through hoops to manage funds and stay compliant… oh wait, they are.

So, let’s break it down, have a little fun, and see what could happen if you take $100,000 and put it to work across different investments over 10 years.

Industry Super vs SMSF: The Basics

Industry Super: The big, comfy blanket. Managed by institutions, diversified across shares, bonds, and other assets, usually includes built-in insurance. Fees are reasonable, averaging about 1% of your balance per year. You put your money in, they do the heavy lifting, and you watch it grow steadily. Nanny has hidden your piggy bank for you. Australia’s super funds manage over 4 TRILLION DOLLARS.

Do you think they have your best interests at heart — or could they be corralled into government shenanigans, green energy deals, and woke agendas?

SMSF: The DIY, take-the-wheel alternative.

You’re the trustee, beneficiary, investor, and compliance officer. Fees are unavoidable — accounting, auditing, and regulatory costs typically start around $3,000–$4,000+ per year, so small balances can feel crushed by costs. But you get full control over investments, from property to gold to niche shares. It’s flexible, hands-on, and sometimes feels like giving the middle finger to Big Brother.

A Little Story: When the System Says “No”

Take Joe, a small-time investor with $80,000 in super and a dream of buying a small commercial property out west. He walks into a few accountants and lawyers, ready to set up his SMSF, only to be met with the same chorus:

“Sorry, mate, your super balance is too low — the fees will eat up your returns, and you probably won’t know how to manage it.”

Joe leaves frustrated, wondering why the ‘professionals’ treats him like he’s incapable of managing his own money. Yet, with some determination, research, and careful planning, Joe could have bought a modest property, collected rental income, and seen his balance grow substantially over time.

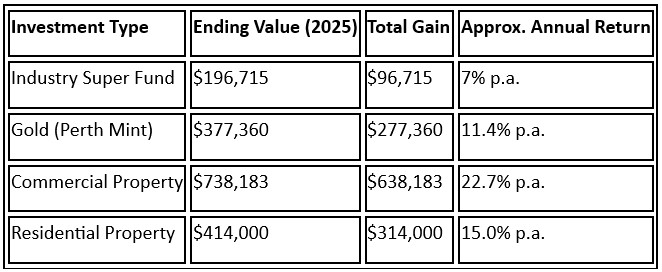

What $100,000 Could Do: A Tale of Four Investments

Let’s see what $100k invested in 2015 could look like today if you were clever (or lucky).

Notes on calculations:• Commercial Property: Bought outright and fixed up for $100,000. Initial rent $23,000/year, indexed at 3% p.a., first 6 months rent-free for tenant fit-out, all outgoings covered by tenant, improvements worth $10,000 remain with property, current value calculated using 6% cap rate.

• Residential Property: $100,000 purchase, weekly rent $275, indexed at 5% p.a., moderate capital growth doubling value over 10 years.

Even a modest residential property beats industry super. Commercial property? A total juggernaut. Gold is great for holding value but doesn’t produce cash flow.

SMSFs: Rules, Risks, and Strategy

SMSFs are powerful — but you can’t just throw money at a property and hope for the best. ATO rules demand diligence:

• Sole Purpose Test: Fund exists only to provide retirement benefits. No personal spending sprees.

• Arms-Length Rule: All transactions with related parties must be on commercial terms. No sweetheart deals.

• Diversification?: Warren Buffett famously says “don’t diversify for the sake of diversifying” — focus on what you know. You might diversify within shares or cash-flow-producing assets, but avoid spreading too thin across things you don’t understand.

Monitoring, diligence, and recordkeeping aren’t optional — they’re your ticket to freedom without penalties.

Cash Flow Trumps Everything

Here’s the golden rule: cash flow is king. Rent, dividends, or other income streams are what keep your fund ticking.

• Property: Rental income plus growth compounds returns like crazy. In our commercial example, even after a 6-month rent-free period, the combination of indexed rent and tenant improvements produces huge total gains.

• Shares: Dividends and franking credits matter.

• Gold: Excellent for value preservation, but no cash flow unless you’re trading it.

Long story short — if your investment produces cash every month, you can reinvest, cover fees, and grow your nest egg faster than any passive fund could.

Not Investment Advice

Before anyone yells at me — this is for entertainment and education purposes only. I’m not your financial adviser, and this article is not investment advice.

Always do your own research, seek professional guidance, and make sure your SMSF or investments comply with all regulations.

Bottom Line

SMSFs aren’t for everyone, but if you’re willing to roll up your sleeves, understand the rules, and focus on cash-flow-producing assets you know well, they can outperform traditional industry super funds — sometimes spectacularly.

Whether it’s gold, commercial property, or a humble residential investment, the magic combo is: knowledge + control + cash flow.

And maybe, just maybe, a little rebellious spirit toward the Big Brother of finance. Beware of anyone who tells you that you won’t be able to understand this or that, or that it’s best left to the experts.

Written by John E Middleclass.

Chitchat Newspaper. November 2025.